The global avocado market has reached a new dimension. According to the latest Rabobank report, its value now stands at around US$20.5 billion, while the number of exporting countries is expanding at an unprecedented pace. In the 2015/16 season, only 12 countries exported more than 5,000 tonnes per year; by the end of this decade, that figure is expected to reach around 30.

The ‘green gold’ fever continues unabated. On the production and marketing side, everyone is eager to capitalise on a product whose consumption keeps growing, with traditional regions leading the market—namely the Americas and Europe—and emerging markets such as Asia and Africa showing strong future potential. From a consumption perspective, global demand appears insatiable. All of this is reshaping the status quo and posing complex challenges across the supply chain, from grower to retail.

Mexico consolidates its dominance

The global avocado leader remains firmly on its throne. Through the Association of Avocado Producers and Exporting Packers of Mexico (APEAM), Mexico manages access to the US market, its main destination, carries out global promotional campaigns and ensures compliance with phytosanitary protocols. Its production capacity allows for large-scale shipments at key moments such as Cinco de Mayo (more than 96,000 tonnes in 2025) and the Super Bowl (110,000 tonnes). This ability to supply at scale remains its main competitive advantage in the face of intensifying competition.

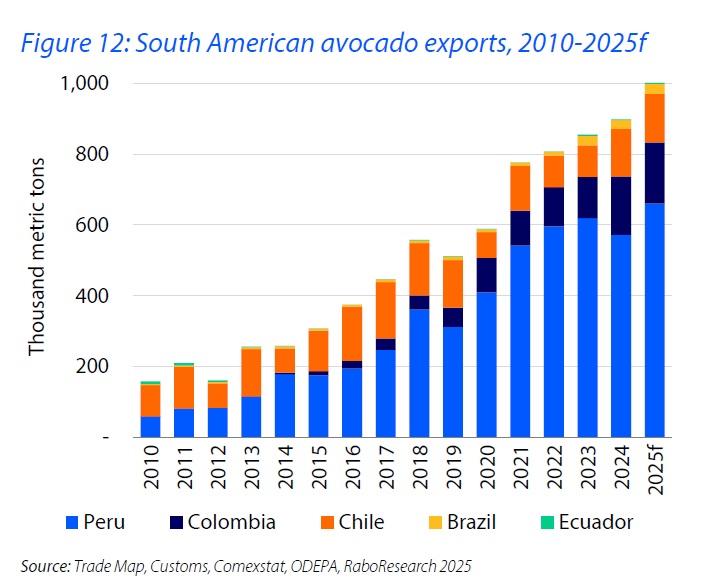

South America’s unstoppable rise

While Mexico defends its position, South America has increasingly established itself as a driving force on the export map. Peru, through ProHass, closed a historic 2025 season with 690,000 tonnes exported (+37% year-on-year), consolidating the country as the second global player. Its strategy is based on destination diversification: Europe absorbed 62% of shipments, while the United States, Japan and China recorded growth of 54%, 73% and 25%, respectively.

Colombia, meanwhile, represents the major bet for the future. According to Corpohass data, shipments to the United States increased by 391%, totalling 9,396 tonnes. The sector report reflects the industry’s focus on its two key markets—the US and Europe—supported by a sustained expansion of cultivated area.

RELATED NEWS: Spanish avocado production expected to grow by up to 30% this season

Chile is the world’s second-largest consumer of Hass avocado, with 8.6 kg per capita per year, and allocates 43% of its production to the domestic market. Nevertheless, its commitment to production and exports continues to grow. In 2024/25, it reached its highest production level in 15 years, at 240,000 tonnes, of which 57% was exported, mainly to Europe (77,000 tonnes), according to the Chilean Avocado Committee.

Saturation, trade policy and sustainability

In this scenario, rising production represents both an opportunity and a risk. In its report, Rabobank warns that the arrival of large volumes in Europe—especially from Peru and African countries—is putting pressure on wholesale prices during peak season. The seasonality of oversupply becomes a real risk, requiring more aggressive marketing strategies to stimulate demand and absorb production peaks.

The geopolitical environment adds further uncertainty, and sustainability has ceased to be a slogan and has become a market access requirement in the most demanding destinations. Initiatives such as APEAM’s “Sustainability Route”, along with origin and quality labels, respond to consumer and retail demand that increasingly prioritises environmental and social criteria.

The race for ‘green gold’ has entered a phase of maturity, in which operational resilience and commercial strategy will determine the difference between winners and those left behind.